9 / Articulation of the extra-financial reporting system (Non-GAAP reporting)

Non-GAAP reporting consists for a company in communicating on the social, environmental and societal implications of its activities as well as on its mode of governance:

• When the company lacks HCM accounting capacity to process human capital data, it lacks the leverage required for its EXTRA-FINANCIAL REPORTING.

The diagram above shows how with HCM accounting technology the company now has the capacity to do what was not technically possible despite regulatory requirements and collective performance agreements or the basis for collective bargaining.

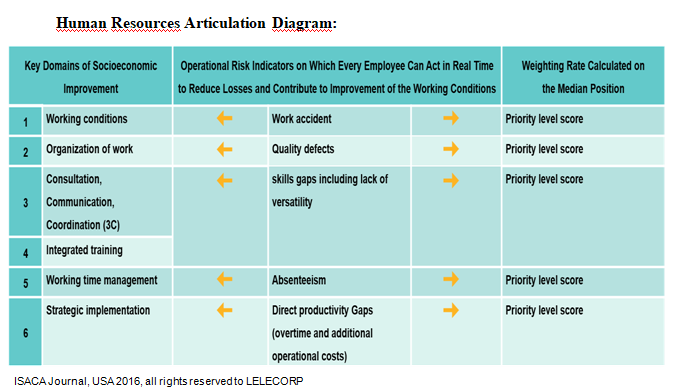

First of all: Improvement of working conditions in real time. Each socio-economic indicator, leveraged on which employees act in real time to improve their financial performance, is measured by the team’s result and remunerated in variable salary according to the weighting ratio assigned to each indicator. It is automatically linked to one of six key areas:

• Physical conditions of work

• Work organization

• Consultation, Communication and Coordination (3Cs)

• Integrated training

• Time management

• Strategic implementation.

Secondly: HCM accounting sub-module of the HRD completes the system by taking into account the axis of psychosocial risks, factors aggravating operational risk losses. The FinTech IRM module of this axis works on the basis of the indicators approved by the Report of the International College of Expertise on the monitoring of psychosocial risks at work published in April 2011 under the title ''Measuring and Controlling Psychosocial Risks at Work'':

• Work requirements

• Emotional requirements

• Autonomy

• Margins of maneuver

• Social and labor relations

• Different value conflicts

• Employment and wages insecurity

The periodic evaluation reports are sent to the general management for prevention and managing work stress.