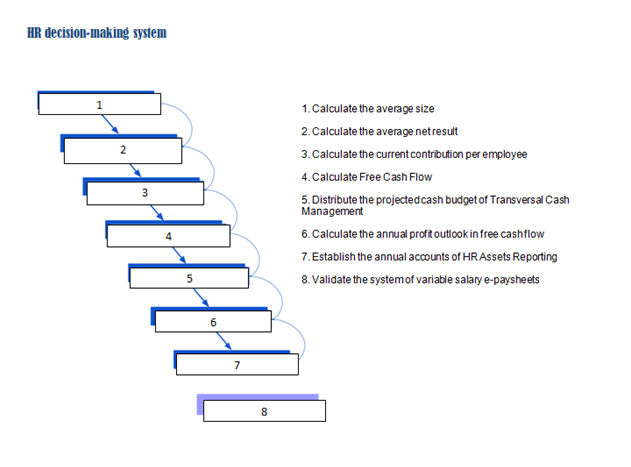

4/ Start by creating your HCM accounting account for a reporting giving a first overview of your projected economic capital gains

This account allows the CEO to access the simulator of forecast management accounts for the Added Value of Human Capital (the total paid workforce) that the Board of Directors needs to make remuneration policy decisions in accordance with laws and regulations governing the context of 100% LCR.

• At this stage, you need this simulator because your internal team, in particular the CFO and the HRD, do not yet have access to the operational management interaction platform to extract and process the historical data of unexpected losses ( UL) and Expected Losses (EL) stored in your internal databases.

• At this point, you can only use the operating income accounts of the last five years to provide the economic gains accounts improving future performance taking into account the added value of human capital.

Your simulation objectives:

• The simulator gives an overview of your future turnover based on the average of past performance. It tells you how to reconcile the management accounts (management accounting) to be entered in the EXTRA-FINANCIAL PERFORMANCE STATEMENT (non-GAAP reporting) with the income statements of turnover in financial accounting or financial information.

• In order to mobilize your social partners and the total employee workforce around a transparent and manageable project of COLLECTIVE PERFORMANCE or COLLECTIVE BARGAINING on the basis of socio-economic indicators within the reach of all employees in accordance with the provisions of the Code du The data processed by the simulator also gives you the future performance accounts of variable salaries separate from the future financial performance accounts linked to the fixed salaries forecast in each year's turnover.

- You thus avoid paying your employees twice for the same performance objective even though the shareholder is not remunerated in the event of a negative result.

This traditional erroneous practice is now prohibited by the laws and regulations governing the context of 100% LCR (See US SEC guidance of April 4, 2018, the European Directive of May 17, 2017 and the laws of other countries).